Kickstart 2026: Your Financial "Fresh Start" Checklist

(And Why This Year is Different for Retirees)

Welcome to 2026! A new year brings a fresh start, but this specific year also brings some major changes to the financial rulebook—particularly for retirement savers and high earners.

Whether you are already enjoying retirement or are in the final stretch of your career, use this checklist to ensure you are not just compliant, but optimizing your wealth for the year ahead.

The Basics: Your "Fresh Start" Foundation

Before diving into complex tax rules, let’s handle the housekeeping. As detailed in our Start of the Year guide:

- Cash Flow Check: Did your income or expenses shift in 2025? Update your budget now to reflect your current reality, not last year's.

- Replenish the Safety Net: If you dipped into your emergency fund for holiday spending or 2025 surprises, make a plan to top it back up to 3–6 months of expenses.

- Reset Your Goals: Are you planning a big family trip or a home renovation this year? Write it down. Your money needs a job to do.

The RMD Spotlight: Rules for 2026

If you were born in 1953 or earlier, pay close attention. The rules for Required Minimum Distributions (RMDs) are in full effect, and the age triggers can be confusing due to recent law changes (SECURE 2.0).

- The "Magic Number" is 73:

- If you turn 73 in 2026 (Born 1953): You technically have until April 1, 2027, to take your first distribution. However, be careful—delaying means you’ll have to take two distributions in 2027, which could spike your tax bill.

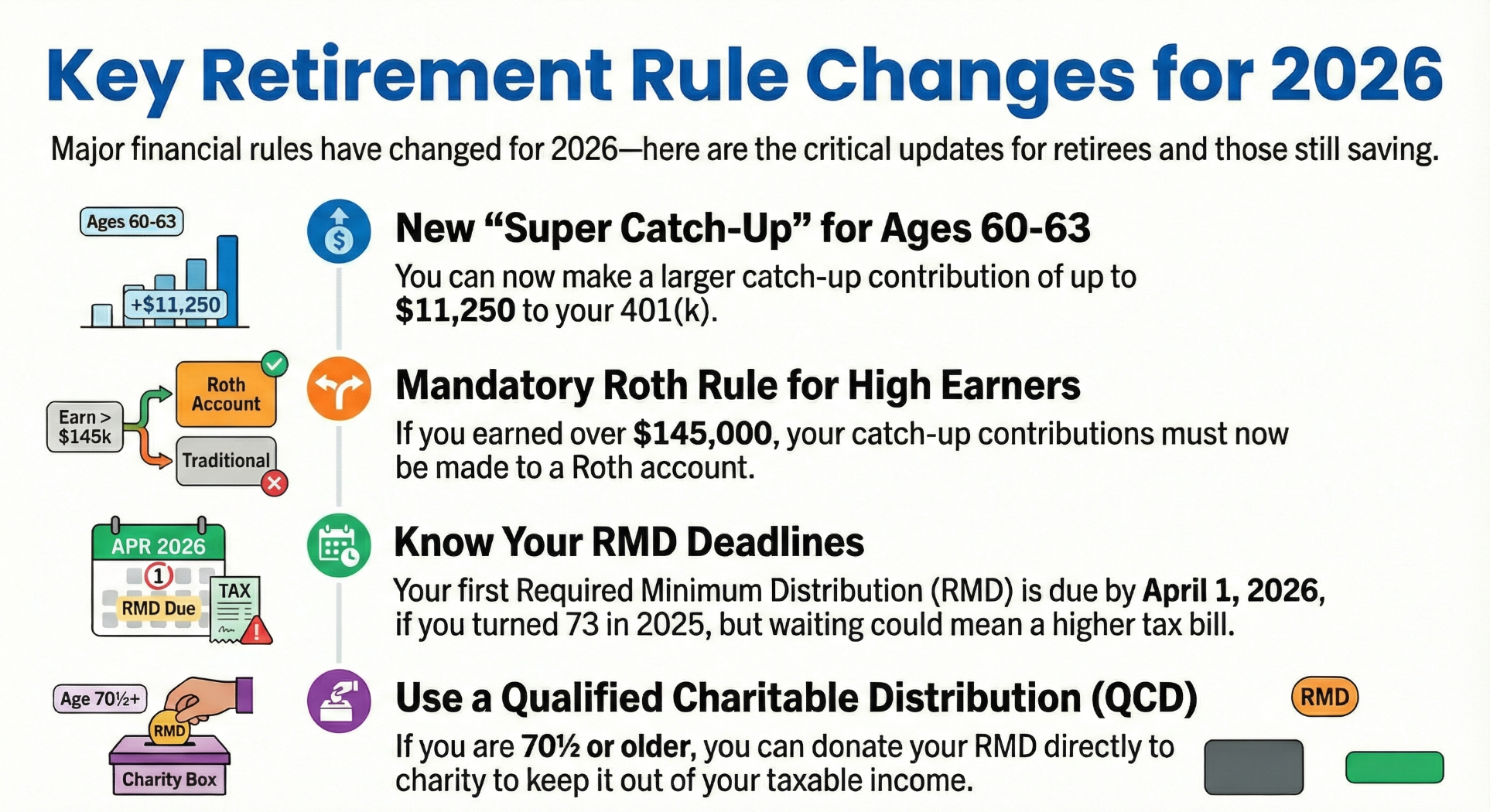

- If you turned 73 in 2025 (Born 1952): Your first RMD is due by April 1, 2026. Your second (for the 2026 year) is due by December 31, 2026. Don't miss these dates—the penalty is up to 25% of the missed amount!

- Strategic Move: The QCD:

- Don't need the cash? If you are 70½ or older, consider a Qualified Charitable Distribution (QCD). You can move funds directly from your IRA to a charity. It counts toward your RMD but stays out of your taxable income—a massive win for tax planning.

New for 2026: The "Super Catch-Up" & Roth Rules

2026 is a landmark year for retirement contribution changes. If you are still working, you need to know this:

- The "Super Catch-Up" (Ages 60-63): If you are between ages 60 and 63 this year, you have a special opportunity. You can now make a "super" catch-up contribution to your 401(k) of up to $11,250 . Combined with the standard $24,500 limit, eligible individuals aged 60-63 can contribute up to $35,750.

- The "High-Earner" Roth Rule: This is a big one. Starting in 2026, if you earned more than $145,000 (indexed) in the previous year, your catch-up contributions must be made to a Roth account. You pay taxes on that money now, but it grows tax-free. Check your pay stub to ensure this is set up correctly!

Estate & Beneficiary Review

Life changes fast. Start 2026 by double-checking:

- Beneficiaries: Did you get married, divorced, or have a grandchild in 2025? Ensure your IRA and insurance policies match your current wishes.

- The "10-Year Rule": Remember, most non-spouse beneficiaries inheriting a retirement account must now empty it within 10 years. This affects how you might want to leave assets to your heirs.